Ghosts on the Payroll: How Gilded Age Financial Records Expose the Architecture of Worker Exploitation

The Gilded Age is remembered, rightly, as a period of extraordinary industrial expansion. Steel mills multiplied across Pennsylvania. Railroad lines stitched together a continent. Textile factories hummed from Massachusetts to Georgia. What the celebratory accounts of that era tend to omit is an equally systematic infrastructure of financial fraud—one that operated in plain sight, encoded in the very ledgers that companies used to document their supposed legitimacy.

For researchers working at the intersection of labor history and archival documentation, those ledgers have become something of a revelation. Payroll records, internal auditor reports, court depositions, and state labor commission filings from the 1870s through the early 1900s are yielding evidence that wage manipulation, ghost employee schemes, and deliberate bookkeeping fraud were not incidental to Gilded Age industry. They were, in many documented cases, built into it.

The Ledger as a Crime Scene

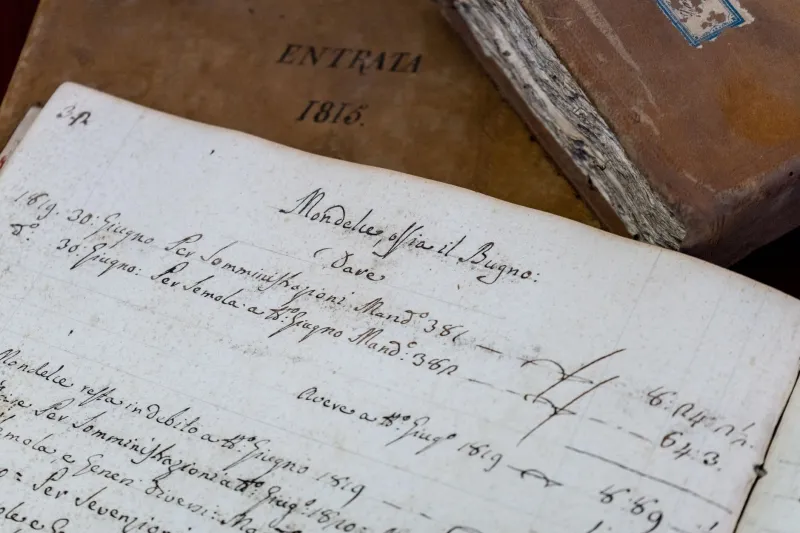

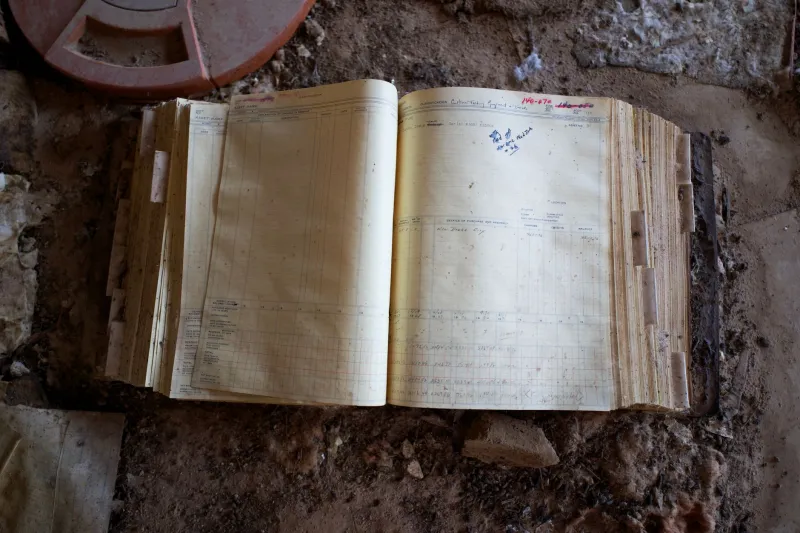

At first glance, a nineteenth-century payroll book appears to be among the driest of historical artifacts. Column after column of names, hours, and dollar figures—handwritten in fading ink, sometimes water-damaged, often incomplete. Yet it is precisely the incompleteness, the irregularity, the entries that don't quite add up, that have drawn the attention of archival researchers in recent decades.

Historians examining records held at institutions such as the Hagley Museum and Library in Wilmington, Delaware—one of the foremost repositories of American business history—have identified recurring patterns of numerical anomaly in industrial payroll documentation. Names appear on weekly tallies for workers who, cross-referenced against company boarding house records or local census data, demonstrably left employment months earlier. Pay rates listed for certain categories of workers shift without explanation between one quarter and the next. Deductions for tools, housing, and company store credit appear to exceed what workers could plausibly have earned in the same period.

These are not accounting errors. They are, researchers argue, the fingerprints of deliberate manipulation.

Ghost Employees and the Foreman's Privilege

One of the most thoroughly documented forms of Gilded Age payroll fraud involved what might be called the ghost employee scheme—a practice in which supervisors or bookkeepers entered fictitious workers onto payroll rolls and pocketed the corresponding wages themselves. The mechanics were straightforward: in an era before standardized employee identification, centralized HR departments, or systematic auditing, a foreman who controlled both the work assignments and the paperwork faced almost no institutional check on his behavior.

Court records from several high-profile fraud prosecutions in the 1880s and 1890s illustrate this dynamic with uncomfortable clarity. In one Pennsylvania railroad case, prosecutorial exhibits introduced into evidence showed that a division paymaster had maintained a roster of fourteen workers whose names appeared consistently on bi-weekly pay sheets across a period of nearly three years. Witness testimony established that none of these individuals had performed any labor for the company during that time. Several had relocated to other states. Two were deceased. The paymaster had, in effect, been paying himself through a network of invented identities.

What makes this case archivally significant is not its uniqueness but its typicality. Similar prosecutorial records from Ohio, Illinois, and Massachusetts during the same period describe structurally identical schemes across industries as varied as textile manufacturing, municipal construction contracting, and coal extraction.

The Scrip Economy and Manufactured Debt

Ghost employees represent only one strand of the fraud documented in these records. Equally revealing are the financial instruments that companies used to transform wages into something closer to controlled credit. The company scrip system—in which workers were paid not in cash but in tokens or certificates redeemable only at company-owned stores—has long been acknowledged by labor historians as a mechanism of economic control. What the archival record adds is granular evidence of how that control was actively manipulated to manufacture debt.

Account books from company stores in West Virginia and Tennessee mining communities, some preserved in state archive collections and others held by university libraries, show systematic overcharging on staple goods and deliberate inflation of tool-rental fees. Cross-referencing these store ledgers against the corresponding payroll documents reveals a pattern: workers who might nominally have earned a living wage found themselves perpetually indebted to the company by the time deductions were applied. The arithmetic was not accidental. Margin notes in several preserved store managers' handbooks suggest that maintaining a specific level of worker indebtedness was considered a management objective, not a side effect.

State labor commission reports from the same period occasionally flagged these discrepancies. A number of such reports, available through digitized state archive collections, include auditor annotations expressing concern about the gap between nominal wages and effective take-home pay. In most cases, the commissions lacked enforcement authority. The reports were filed. The practices continued.

What the Auditors Knew—and Didn't Say

Perhaps the most instructive documents in this archival constellation are the internal audit reports that large industrial firms commissioned during the Gilded Age. These were not public documents. They were produced for corporate leadership and were, in many cases, deliberately withheld from shareholders and regulators alike. The survival of such materials in business archives is therefore something of an accident of history—the result of corporate mergers, bankruptcy proceedings, and estate settlements that transferred private records into institutional custody.

What these audits reveal is that senior management frequently had contemporaneous knowledge of payroll irregularities and chose not to act on them. In several documented cases, the auditor's findings were summarized, noted as requiring attention, and then quietly archived without any corresponding corrective action. The fraud was known. It was documented internally. And it was allowed to continue.

This pattern has significant implications for how historians interpret the labor conflicts of the era. When workers struck over wage disputes in the 1880s and 1890s, they were often dismissed in the press as agitators making unreasonable demands. The internal financial record tells a different story—one in which workers' grievances about pay were, in at least some measurable proportion of cases, responses to documented fraud rather than expressions of abstract discontent.

Recovering What Was Buried

The challenge facing researchers today is not simply one of access, though that remains real. Many relevant records are fragile, poorly indexed, or held in collections that lack the processing resources to make them fully searchable. Digitization initiatives at institutions including the Library of Congress, various state historical societies, and university special collections have made meaningful progress, but the documentary landscape remains uneven.

Methodologically, the work requires a kind of triangulation—matching payroll data against census records, court filings, labor commission reports, and newspaper coverage to build a composite picture that no single document type could provide alone. This is painstaking work, and it is ongoing.

But the payoff, in terms of historical understanding, is substantial. The Gilded Age is often narrated as a story of industrial triumph shadowed by labor unrest. The archival financial record suggests a more precise framing: it was a period in which the mechanisms of worker exploitation were institutionalized, documented in real time by the companies that practiced them, and then carefully buried in the files. The ledgers survived. The workers' stories, encoded in those columns of numbers, are only now beginning to be fully read.

For historians, that is precisely what archives are for.